-

The Role of the Ukraine Conflict on EU Energy Policy: Seeking Solutions to Energy Dependency

Simge Pelit

Received: 03 Apr 2026 | Revised: 12 Jun 2026 | Accepted: 15 Jun 2026 | Published online: 16 Jun 2026

How to cite this article: Pelit, S. (2026). The role of the Ukraine conflict on EU energy policy: seeking solutions to energy dependency. Global Geopolitics. Advance online publication. https://doi.org/10.64901/29778271.2026.013

DOI: 10.64901/29778271.2026.013

AbstractHow has the Ukraine conflict affected the European Union’s energy security policy? By adopting an interpretive approach and a comparative assessment of the pre-conflict and post-conflict periods, the article aims to investigate the shifts in the EU’s energy security strategy after the eruption of the conflict and to assess the extent of its reliance on Russian natural gas. The study finds that the Ukraine conflict transformed EU energy security from a strategy centered on external energy dependence into one increasingly focused on diversification, resilience, renewable energy, and strategic autonomy, revealing the need for a broader restructuring of the Union’s energy system.Keywords: energy security; European Union; natural gas; Russia; Ukraine conflictIntroduction

Recent geopolitical turbulence has brought energy security to the forefront of the global agenda. One of the most prominent examples of these crises is the Ukraine conflict, which caused not only a military and political crisis but also large-scale disruptions in energy markets. This conflict is regarded as a turning point, particularly for the European Union (EU), which exposed vulnerabilities in energy supply and reignited discussions about energy security.

Since the 2000s, the EU had deepened cooperation with Russia as a means of securing uninterrupted energy supply. This increasing interdependence made Russia the EU’s primary supplier of natural gas. However, over time, this relationship became increasingly asymmetrical as dependence on Russian gas reached critical levels. The gas shortages of 2006 and 2009 uncovered the weaknesses of the EU’s energy strategy and heightened concerns about energy security. Even though these disruptions could be regarded as wake-up call, the EU did not take sufficiently concrete and effective measures to diversify supplies until the start of the Ukraine War.

After the conflict in Ukraine broke out, the EU, in the spirit of solidarity, decided to impose sanctions on Russia. Yet, this decision turned out to be a double-edged sword. Restrictions imposed on Russian gas exports led to a sudden spike in energy prices (Muhibbin et al., 2025, pp.520-521). Sudden increases in energy prices and fluctuations in energy markets have created significant costs for EU economies, leading to economic difficulties in many European countries and placing energy security even higher on the EU's list of strategic priorities. Energy crisis, which exposed vulnerabilities and excessive external dependence, reestablished the EU’s priorities of strategic autonomy and energy security (Roa, 2026, p.1). Ukraine’s strategic importance as an energy transit country, together with Russia’s use of energy resources as an instrument of foreign policy, further underscored how costly and risky this dependence can be. As Osička and Černoch (2022) put it “Once again, energy geopolitics is making the headlines,” and developments accelerated the EU’s attempts to diminish its heavy reliance on Russian natural gas and diversify energy supply routes.

In this regard, this article asks: How has the Ukraine conflict affected the European Union’s energy security policy, particularly in terms of changes in its dependence on Russian natural gas and the measures adopted to reduce that dependence? By adopting an interpretive approach and a comparative assessment of the pre-conflict and post-conflict periods, the article aims to investigate the shifts in the EU’s energy security strategy after the eruption of the conflict and to assess the extent of its reliance on Russian natural gas. While existing studies have examined EU-Russia energy relations in relation with the concept of energy dependence, this article contributes the literature by demonstrating how the Ukraine conflict accelerated changes in EU energy policy and exposed the limits of earlier efforts to ensure energy security.

The study consists of three main sections. The first section provides an overview of the key concepts related to energy security, energy dependence, and price volatility. The second section elucidates the formation of EU energy policy prior to the conflict and examines the historical trajectory of its dependence on Russian gas. The third section reviews the measures implemented after the outbreak of the conflict, the policies implemented to reduce dependence, and the short-term outcomes of these measures. The conclusion gives a summary of the main findings and offers an evaluation of the policies the EU is likely to pursue in the long run.

Conceptual Framework

Energy dependence and energy security are two closely related concepts that are essential for understanding the extent to which states rely on energy imports to satisfy their energy needs and the risks associated with this dependence. The growing significance of these concepts has been further amplified due to the shifts in supply and demand balances in global energy markets, together with price volatility and geopolitical tensions in the world. Countries that rely heavily on external energy suppliers becomes more vulnerable to supply disruptions and price fluctuations, which can directly affect economic development and national security. This section clarifies the fundamental concepts of energy security, energy dependence, and price volatility.

First, it is essential to explain the concept of energy security, which constitutes the central concept of this discussion. This concept entered into the literature after the oil crises of the 1970s, which exposed the high level of reliance on imported hydrocarbons. In order to curb the power of oil cartel, the West came up with the strategy of interdependency of oil markets (LaBelle, 2024, p.1). The foundation of International Energy Agency (IEA) in 1974 was a protective measure to prevent the occurrence of another such crisis (Roa, 2026, p.4). Laying the groundwork, energy security is defined by the measures taken to ensure energy supply and is based on three main criteria: reliability, affordability, and continuity of supply (IEA, n.d.; Azzuni & Breyer, 2018, p. 3). Reliance on only a few suppliers and fixed infrastructure in energy supply exposes markets to imperfect competition and dependency dilemmas. Energy security, as conceptualized by Daniel Yergin (2006), is “the availability of sufficient supplies at affordable prices.” This description parallels that of the IEA, which explains it as “the uninterrupted availability of energy sources at an affordable price.” Similarly, Gawdat Bahgat (2006) characterizes energy security as a consistent supply at reasonable prices.

The IEA (2019) approaches energy security from two dimensions. In the short term, it means the capability to react quickly to sudden supply and demand changes. In the long run, it emphasizes the need for timely investments to meet economic development and environmental requirements. A failure to diversify energy sources and dependence on existing infrastructure weaken energy markets and expose them to vulnerabilities that undermine the security of supply.

Energy dependence is another key term that plays a significant role in this case. It refers to the extent which an economy relies on imported energy supplies as a means to fulfil its domestic energy demand (Eurostat, n.d.; Sözen, 2009, p. 4827). For countries seeking to ensure energy security must address challenges such as energy dependence, price volatility, resource scarcity, and environmental concerns in the short term. In the long term, they must consider issues such as the energy investment and the political stability of supplier countries (Carfora et al., 2022).

The last concept to be examined in the conceptual framework section is price volatility. Simply put, it indicates the pattern of price movement of a commodity in terms of magnitude and frequency over time. For price volatility, what matters here is not the price level itself but the degree of change. Volatility presents supply-demand imbalances in the market and reveals the extent to which prices fluctuate (U.S. Energy Information Administration, 2022). As a fundamental energy sources, natural gas and electricity are more subject to volatility than other commodities. This is mainly because most consumers cannot afford to switch to other fuels due to price changes (IEA, 2022).

In this context, the sharp surge in natural gas prices that occurred with the eruption of the 2022 Ukraine conflict is a clear example of price volatility. The EU found itself more severely affected than other regions during this time. The extent of dependence on Russian gas became much clearer when Russian gas deliveries were limited. This triggered necessary changes in EU energy policy to support greater strategic autonomy. The subsequent section will present a comprehensive assessment of the interplay between Russian gas dependence and EU energy policy over time.

The Trajectory of EU Energy Policy and Russian Energy Dependence

The Development of EU Energy Policy

EU energy policy has gone through considerable changes over time, influenced by both economic integration and rising environmental concerns. The roots of this cooperation were laid when the European Coal and Steel Community was formed under the Treaty of Paris in 1951. Shortly after, the Treaty of Rome in 1957 further strengthened collaboration within the field of energy. When the EU (then European Community) started shaping its energy policy, its first and foremost objective was to ensure supply security at an affordable price (Güven & Güneş, 2020, p. 272).

In its formative years, concerns about energy supply were on the top of the agenda. However, the national energy markets that adopted protectionist policies during that time, remained largely isolated from one another. In the wake of the 1973 oil crisis, concerns about supply security grew among European leaders, which clearly indicated the need of a more coordinated approach. Came into force in 1987, the Single European Act was considered as a significant step toward deepening integration and reducing obstacles to energy trade across borders. In the following years, the 1992 Treaty on European Union and the 1997 Amsterdam Treaty underlined the prominence of energy supply security and market regulations (Tekin & Williams, 2011, p. 13).

During the 1990s, EU energy policy placed growing importance on climate change. The Intergovernmental Panel on Climate Change (IPCC)’s first assessment report and the 1997 Kyoto Protocol provided a basic for formulating a coherent and unified approach to both climate change and energy security (Kanellakis et al., 2013, p. 1020). These developments accelerated efforts to integrate environmental sustainability into the Union’s energy policy.

Effective from 1998, the Energy Charter Treaty was a multilateral agreement designed to foster international cooperation and creating an open energy market. The treaty contains provisions on dispute settlement, protection of investment, energy transit and trade. This development led the European Commission to extend its regulatory authority to the Union’s energy interactions beyond its own borders (Energy Charter Treaty, 2016, p. 2; Yafimava, 2011, p. 109). The Green Paper published in 2000 “Towards a European Strategy for the Security of Energy Supply” emphasized the growing importance of natural gas as a relatively cleaner alternative to oil (Sauvageot, 2020, p. 9).

The strategy “An Energy Policy for Europe,” adopted in 2007 and established three cornerstones of EU energy policy: competitiveness, security of supply, and sustainability. It set targets to be achieved by 2020, reaching a 20 percent renewable energy share in overall energy consumption, improving efficiency by 20 percent, and a 20 percent cut in greenhouse gas emissions (Kanellakis et al., 2013, p. 1021).

The Lisbon Treaty, effective since 2009, introduced a new aspect to EU energy policy by making the regulation and integration of energy markets an EU wide priority. The treaty assigned the EU responsibilities such as ensuring energy security, encouraging energy efficiency, promoting the effective operation of energy markets, and supporting the energy networks coordination. It also emphasized solidarity among member states as a key principle in moments of crisis (Lisbon Treaty, 2008).

The EU’s prosperity, security, and stability depend on uninterrupted supply of energy. Since the 1970s oil shocks, most EU countries had not encountered a prolonged disruption in energy supply. As a result, energy was widely perceived as a resource that was always accessible without difficulty. The disruptions in Russian gas supplies in the winters of 2006 and 2009 changed this perception (Chow, 2009). Some member states, especially in Eastern Europe, were seriously affected. These gas crises showed the EU’s sensitivity to unexpected energy shocks and clearly emphasized the necessity of a unified European energy policy. From this period onward, the EU adopted various measures to bolster its energy security and to lower the number of states that were relied on single provider (European Commission, 2014).

Data from the Statistical Office of the European Union (Eurostat, 2022a) show energy dependency of the EU until 2020. According to these data, the EU remained highly dependent on energy imports throughout 2010–2020, with oil dependency consistently around 93–97% and natural gas rising from roughly 68% to nearly 90% by 2019 before dropping slightly to the mid-80s in 2020. Overall dependency increased from about 55% to around 60% by 2019, while solid fossil fuels fluctuated between roughly 38–44% before declining sharply to about 36% in 2020. Based on these figures, one could conclude that the disruptions encountered in 2006 and 2009 were not actually a sufficient wake-up call for the EU.

Building on these developments, the European Commission issued the “European Energy Security Strategy” in May 2014 (COM(2014) 330 final). The document emphasized that 53 % of the EU’s energy consumption relied on imports. It noted that import dependence reached 40 % for nuclear fuel, 42 % for solid fuels, 66 % for natural gas, and 90 % for crude oil. While acknowledging that energy supply security was more sensitive for certain member states, the Commission underlined its importance for all member states and drew particular attention to dependence on Russia (European Commission, 2014). Therefore, the new strategy promoted diversification, stronger interconnections, and accelerated renewables development to reduce dependency (Roa, 2026, p.6).

Approximately six months later, on 25 February 2015, the “Energy Union Package” (COM(2015) 80 final, 2015b) was published, providing a legal footing and principles for energy security. Accordingly, the energy policy is grounded in five main objectives: 1. To diversify energy sources to guarantee security through EU solidarity and cooperation. 2. To develop an integrated internal energy market by removing infrastructure and regulatory barriers. 3. To increase energy efficiency, lower emissions, reduce dependence on imports, and promote economic growth. 4. To decarbonize the economy by aligning with the Paris Agreement and facilitating the move towards a low carbon future. 5. To prioritize innovation and support research in clean energy technologies so as to enhance competitiveness and advance the energy transition (European Parliament, 2024).

The launch of the Energy Union demonstrated the intention of a more systemic and integrated approach of the EU. The objectives put forward were aligned with the Paris Agreement. It was basically a call for a shared strategic vision for EU energy policy built on decarbonisation, supply security, energy efficiency, innovation, and market integration (Roa, 2026, pp.5-6).

Eurostat (2022b) data reveal that that remained the dominant supplier of the EU’s primary energy imports throughout 2010–2020, with its share rising significantly in hard coal from around 22% to nearly 49%, while remaining consistently high in natural gas (roughly 30–40%) and crude oil (around 26–35%). At the same time, the data indicates gradual diversification, particularly with the increasing role of the United States in crude oil (from near 0% to about 8%) and natural gas (rising to around 6% by 2020), although these shifts did not substantially reduce overall dependence on Russian energy.

A proposal for a regulation aimed at safeguarding the natural gas supply was published in 2016. The aim of this proposal was to ensure that the Union was prepared for potential supply disruptions or exceptionally high demand, and to activate the necessary tools in times of crises (European Commission, 2016). Adopted in 2017, regulation (EU) 2017/1938 provided a framework designed to improve the preparedness of the EU in emergency situations and to make it more resilient in the event of gas supply interruptions. Its key provisions included the development of emergency plans, regional cooperation among member states to assess common supply risks, and the establishment of bidirectional capacity across all cross-border gas interconnections (European Commission, 2026).

The impetus for this regulation was the 2014 annexation of Crimea by Russia and its backing of secessionist movements in the Donbas region. As Russia’s threat became more evident, the EU was compelled to adopt rapid and effective measures. However, as shown in Table 1, over the period from 2010 and 2020, the EU’s imports of Russian gas remained relatively unchanged. Despite strategies and regulatory initiatives, dependence could not be reduced, and diversification was not fully achieved. Consequently, from 2014 onward, the European Commission began publishing reports every two years assessing trends in European and international energy prices.

Dependency on Russian Gas Supplies

Energy dependency of the EU on Russia became particularly evident in the 2000s. During this period, the EU deepened its economic and political relations with Moscow in order to ensure energy supply security and to support diversification efforts. The beginning of this process is generally considered to be the Joint Declaration signed at the October 2000 Summit between the EU and Russia (European Commission, 2000). Russia’s natural gas shipments to the EU significantly increased after this declaration established the groundwork for collaboration in the field of energy.

After the collapse of the Soviet Union, Ukraine became a major hub through which more than 80% of Russian natural gas exports passed. Previously controlled by Moscow, the gas storage facilities were now located inside Ukrainian borders. Ukraine's Naftogaz and Russia's Gazprom found themselves locked in a cycle of recurring conflicts during the 1990s and 2000s over gas contracts, debt payments, and the uninterrupted transit of gas to Europe. These tensions reached their peak first in 2006 and again in 2009 when disruptions occurred in gas supplies to Europe during periods of severe winter weather (Skalamera, 2015, p. 400).

The construction of the Yamal-Europe pipeline via Belarus and the launch of the Blue Stream pipeline, which links Russia to Türkiye across the Black Sea, led to a decline in natural gas flows through Ukraine. The proportion of Russian gas transported to Europe via Ukraine stood at around 78% in 2004; this figure fell to 70% in 2008 and dropped to around 60% in 2009 and 2010 due to the financial crises. The Yamal-Europe pipeline was considered a strategic infrastructure asset for EU countries, given the redirection of the gas shipment that previously passed through Ukraine. Nevertheless, its strategic significance diminished with the opening of the Nord Stream pipeline (Sauvageot, 2020, p. 3).

Nord Stream is made up of two pipelines linking Russia and Germany beneath the Baltic Sea, with the capacity to transport 55 billion cubic meters (bcm) annually. The pipeline became operational in 2011 and 2012. Enabled by this infrastructure, the redirection of natural gas transit to bypass Ukraine has diminished strategic leverage of Ukraine as a transit country in the European energy architecture. Hence, Ukraine’s share of Russian gas transit to Europe dropped below 50% because of these events. Natural gas flows in 2021 were 40 bcm via Ukraine, 33 bcm via Yamal, and 55 bcm via Nord Stream (Toth et al., 2020, p. 2; Sauvageot, 2020, p. 3).

Despite the significant decline in transit share, Ukraine remained the main route for Gazprom’s natural gas deliveries to Europe. Even with the strained relations and energy-based conflicts between Ukraine and Russia, the EU’s dependence on Gazprom for natural gas has continued unchanged. According to 2020 data, imports covered around 60 percent of the EU's total energy needs, with a particularly high level of external dependence in natural gas and crude oil. Data from the same year indicate that Russia supplied more than 25% of the crude oil imports (113 million tons), over 40% of its natural gas imports (155 bcm), and more than 50% of its solid fuel imports (44.2 million tons) to the EU (Eurostat, 2022c).

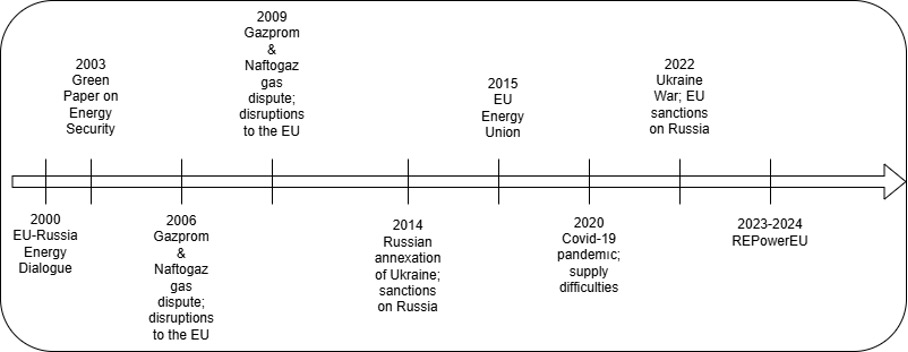

Figure 1: EU-Russia Energy Timeline (Source: Author’s creation) In other words, a conflict between Russia and Ukraine is not a surprise given the relatively recent crises in 2006, 2009, and 2014. These crises underlined the fragile state of the EU’s energy security and served as an opportunity to build a more integrated energy policy. Before the conflict, Russia occupied the top position among the EU’s external suppliers of oil, coal, and gas, with some member states, such as Germany, being highly exposed (Deirmentzoglou et al., 2024, p.2). Russian usage of its energy sources and power to threaten EU states that support Ukraine was the final straw. The 2022 gas crisis revealed the dangers of relying heavily on one supplier and stressed the necessity of source diversification to be flexible and resilient.

Diversification Efforts in Gas Supply Until 2022

It should be noted that, until the outbreak of Ukraine conflict, the EU had been working to make its infrastructure more resilient, ensure price stability, and strengthen energy security through supplier and source diversification. The Union had been aware of the weaponization of Russian gas for years. Hence, it has undertaken various initiatives to identify and construct new routes to decrease its dependence on one supplier for natural gas as well as other energy resources. The Southern Gas Corridor is the first of these initiatives developed for Southeast European countries that are relying on one supplier, with the intention of transporting gas from the Caspian Basin to the EU. It became operational towards the end of 2020 as a new supply channel and delivered 8.1 bcm of gas in 2021 and 11.4 bcm in 2022 to Europe, accounting for approximately 3% of the EU’s overall gas imports (European Commission, n.d.).

Another initiative that deserves attention is the establishment of a gas hub located in the Mediterranean region. In this respect, the EU is engaged in strategic-level energy partnership with Eastern Mediterranean and North African countries. Along with Algeria’s gas reserves, the Eastern Mediterranean's potential as a key energy provider and transit region for the EU has grown due to recent discoveries and infrastructure investments. Owing to their substantial offshore gas deposits, Israel, Egypt, and Cyprus in particular are regarded as the EU's strategic partners in its attempts to diversify its energy supply lines. Several infrastructure initiatives, including the Cyprus EastMed Pipeline and the CyprusGas2EU liquefied natural gas (LNG) terminal, are being planned to enable gas transportation from the region to the EU (European Commission, n.d.). To put it briefly, the Mediterranean region emerges as a strategically important zone for natural gas supply, offering the EU a diverse mix of pipeline and LNG supply channels.

Lastly, the role of the LNG terminals must be addressed. As a diversification source, LNG plays a key role in promoting competition and reinforcing supply security in the gas market. 2016 LNG Strategy by the European Commission (COM(2016) 49 final) designed to foster competition in the gas market and enhance supply security by supporting the development of LNG terminals. The entry of new gas supplies from North America, Australia, Qatar, and East Africa into the global market has led the EU to acknowledge the need for significant interconnection projects to alleviate existing internal bottlenecks and enable access to LNG across the region. To encourage this further, certain LNG regasification facilities in the Baltics and Southeast Europe have been recognized as Projects of Common Interest (European Commission, n.d.).

The data presented here underline how the European Energy Security Strategy places a high priority on supply security. Despite this priority, the measures adopted before the outbreak of the conflict proved insufficient to realize the ambition of diversifying energy sources and suppliers. The result was a long-standing imbalance in EU-Russia energy relations that persisted until the outbreak of the war.

The Trajectory of EU Energy Policy and Russian Energy Dependence

The Ukraine conflict has significantly changed the EU’s economic, political, and diplomatic landscape. The direct consequences of Russia’s attack on Ukraine were felt in European energy markets and global energy prices, with supply uncertainty raising and gas prices climbing to record levels. Until mid- 2021, gas prices remained relatively stable at below €50 per megawatt-hour (MWh), but this is short-lived, as prices skyrocketed to €339.20 by the end of the year. It is essential to point out that the sharp increase is not only due to the invasion of Ukraine but is also driven by supply shortages linked to the restructuring of supply chains, rising demand following the lifting of COVID-19 restrictions, and rising inflation.

The EU took a strong stand against Moscow's actions despite these unfavourable circumstances. European Commission President Ursula von der Leyen articulated her thoughts saying “We must become independent from Russian oil, coal and gas. We simply cannot rely on a supplier who explicitly threatens us” (European Commission, 2022c). During the European Parliament plenary session held on 1 March 2022, it was emphasized that the EU should significantly decrease its energy reliance on Russia; on 7 April 2022, a call was made for the imposition of a swift and comprehensive embargo of all energy imports from Russia including natural gas, oil, coal, and nuclear fuel. Moreover, the attention was drawn to the necessity of completely abandoning the Nord Stream pipelines (European Parliament, 2023b, p. 2).

EU gas prices hit an all-time high in August 2022, rising by 1000% compared to earlier decades. Throughout the last decade, prices had fluctuated between an average of €5/MWh and €35/MWh, but in August 2022 they exceeded €300/MWh, reaching an all-time high. Notably, gas prices between 22 and 26 August 2022 stood at or above €265/MWh for five consecutive trading days (European Commission, 2026). A comparison of natural gas prices in the U.S., Japan, and Europe can be seen in World Bank data (World Bank Blogs, 2025), which European natural gas prices experienced a sharp and unprecedented spike in 2022, rising to around $70/mmbtu, far exceeding levels in the United States (generally below $10/mmbtu) and Japan (peaking around $20–25/mmbtu). Following this peak, prices in Europe declined significantly and gradually converged toward levels observed in other major markets, although remaining comparatively more volatile. What stands out most is the dramatic price escalation in Europe in 2022, which exceeded the prices seen in the U.S. and Japan. After reaching this peak, European gas prices began to decline and gradually approached levels similar to those in other countries.

Despite these difficulties, EU members managed to act collectively to face the problem of excessive prices and market imbalances in the energy sector. This response showed how the Lisbon Treaty's solidarity principle was invoked actively during the energy crisis. It was considered necessary to act collectively for the purpose of mitigating the impact of the crisis and reduce associated risks. LaBelle (2024) highlighted that Europe has moved into a new era free from Russian resources, where a new understanding of energy security emerged based on security, sovereignty, and solidarity.

Approximately one month after the eruption of armed conflict, EU members convened at an informal summit and adopted significant decisions. At this summit, in conformity with the EU’s 2050 climate targets, the focus was placed on invasion of Ukraine by Russia and the gradual move away from Russian energy imports. The Versailles Declaration adopted at the end of the summit included key objectives such as decreasing reliance on fossil fuels, promoting renewable energy and hydrogen technologies, expanding supply diversity (including LNG), strengthening network integration, and increasing energy efficiency (European Commission, 2026).

The EU has started to promote strategic autonomy amid growing global instability and gave rise to the new approach centred on resilience and solidarity (LaBelle, 2024; Roa, 2026, p.2). In May 2022, the European Commission announced the REPowerEU plan in response to growing calls to reduce Russian energy imports. Within the framework of this plan, an EU Energy Platform based on voluntary participation was established, and new agreements were signed with international partners to increase energy supply. This strategic step includes the pursuit of a more varied energy supply, the growth of renewable energy production and strengthening energy efficiency to build a more independent system (Muhibbin et al., 2025, p.523).

In this context, LNG shipments from Canada and the United States to the EU increased, additional natural gas was secured from Norway, new deliveries were planned from Israel and Egypt, and energy cooperation with Azerbaijan was strengthened. The European Council, in December 2022, reached an agreement on a market mechanism aimed at controlling natural gas prices, and a few months later, Member States decided to extend the voluntary target of reducing gas demand by 15%. The Council officially approved this target in March 2023 (European Commission, 2026).

World Bank data (World Bank Blogs, 2025) demonstrate that, unlike other regions, Europe experienced a consistent decline in natural gas consumption over the 2021–2023 period, with particularly sharp reductions of around 80–100 bcm at the peak of the adjustment phase. Although consumption began to partially recover thereafter, it remained below pre-crisis levels, indicating a sustained shift toward demand reduction. Accordingly, the EU recorded a significant decline in natural gas consumption over this period, in contrast to other regions where consumption generally increased or fluctuated.

Additionally, EU members continue to adhere to the objectives of the Green Deal, seeking to lower greenhouse gas emissions while reaching climate neutrality by 2050. In this context, efforts to reshape the Union’s energy policy by replacing fossil fuels with cleaner energy alternatives remain a work in progress. The central goal of the green transition is to diminish the EU’s consumption of and reliance on fossil fuels, protect the environment, ensure a healthier living environment, and enhance energy security. In March 2023, the European Council made progress on a series of proposals under the Fit for 55 package, which seeks to cut net greenhouse gas emissions by 55 % by 2030. These proposals include not only the revision of regulations concerning energy efficiency and renewable energy but also the establishment of a hydrogen and decarbonised gas market (European Commission, 2026).

Meanwhile, the EU has continued to take steps to reinforce the resilience of its energy security. The European Council decided to adopt emergency policies to ensure gas supply during the cold season and to reduce gas demand across the EU. The Council, in June 2022, adopted a new regulation on gas storage and agreed on filling storage facilities before the winter season (European Commission, 2026). During the 2022/2023 winter period, contrary to initial expectations, the energy supply situation proved to be more favourable. Thanks to the EU’s attempts to save energy, gas demand remained lower compared to previous years, while the significant increase in LNG shipments largely compensated for the decline in Russian supplies (European Parliament, 2023a).

An assessment of the strategies developed by the EU as a reaction to the gas crisis emerged after the Ukraine conflict reveals several key objectives, including diversifying supply sources, reducing demand, increasing gas storage capacity, and promoting renewable energy production. In the short term, particular emphasis must be placed on diversifying supply sources. With the intention of ensuring a sustainable natural gas supply, the EU must diversify both its LNG and pipeline gas imports from non-Russian sources (European Commission, 2022b, p. 3).

An analysis of the following graph shows that the proportion of the EU’s non-Russian suppliers has increased. Russian pipeline gas, which once made up 41% of the EU’s total energy imports in 2021, fell to approximately 8% by 2023. To compensate this gap, the EU imported American LNG, which represented 46% of the EU’s LNG imports in 2023, as well as pipeline gas from Azerbaijan (7%), North Africa (19%), and Norway (49%) (European Commission, 2024).

European Commission data (European Council, 2023b) show that EU gas supply sources changed markedly between 2021 and 2023, with the most significant trend being the sharp decline in Russian gas—from roughly 150 bcm in 2021 to around 40 bcm in 2023. This reduction was largely offset by increased imports from Norway (rising to approximately 100 bcm) and the United States (around 60–70 bcm), while North Africa and other suppliers also contributed to diversifying the overall supply mix.

As previously mentioned, the EU has taken meaningful steps to increase its gas supply and lower reliance on only one supplier. In this context, the completion of the Southern Gas Corridor through the integration of the TANAP (Trans-Anatolian Gas Pipeline) and TAP (Trans Adriatic Pipeline) projects has made it possible to supply Europe natural gas from Azerbaijan, thus providing an important contribution to reduction of energy dependence and helping to guarantee a more secure and diverse energy supply for the EU.

In addition, the EU continues its attempts to establish a Mediterranean gas hub by developing partnerships with Algeria, Israel, Egypt, and Cyprus, all of which possess substantial offshore gas reserves. Furthermore, new LNG imports from East Africa, Qatar, and North America have expanded the EU’s gas supply options. To support the integration of these new sources, the EU aims to create a more integrated and resilient energy market across the region by investing in key infrastructure improvements, particularly interconnectors and regasification units in the Baltic region and Southeast Europe (European Commission, n.d.).

Eurostat data (Eurostat, 2026) show that Norway is the EU’s largest supplier of natural gas in 2025, accounting for approximately 52% of imports, followed by Algeria (around 15%) and the United Kingdom (about 13%). Russia’s share has declined significantly to roughly 10%, while Azerbaijan contributes about 8%, reflecting a substantial diversification of supply and a marked reduction in reliance on Russian gas.

Gas storage has become a vital part of the Union’s energy security strategy. Regulation (EU) 2022/1032, adopted in June 2022, required that 80% of the EU’s gas storage capacity be filled by 1 November 2022; this target was later revised to 90% for the years that followed. Due to the rapid adoption of the new regulation by EU members, the filling level of EU storage facilities reached 90% by October 2022 (European Parliament, 2023b, pp. 1–2). Gas Infrastructure Europe data (European Council, 2026) show that EU gas storage levels increased significantly after 2021, with peak filling rates reaching around 90–100% in 2022, 2023, and 2024, compared to roughly 80–85% in 2021. Although storage levels declined somewhat in 2025—falling to around 60–70% by the end of the cycle—they remained above 2021 levels, indicating a sustained improvement in storage capacity and preparedness.

Gas storage facilities are essential for ensuring gas supply security over short periods. Most EU members possess gas storage facilities in their own countries. The large portion of the EU’s natural gas storage capacity is located in the Netherlands, Austria, France, Italy, and Germany. In the absence of domestic storage facilities, member states must store 15% of their annual domestic gas consumption in facilities located in other EU countries and must have access to the gas reserves held there. This mechanism strengthens the EU’s supply security and ensures burden-sharing in financing the filling of storage facilities. Moreover, states with more limited storage capacities cooperate with countries that have larger storage infrastructure to ensure the security of their reserves (European Council, 2024).

The EU adopted gas storage rules in June 2022 (EU/2022/1032) to protect the security of gas supply and lessen the burden of high energy costs following the disruption caused by Russia's offensive against Ukraine in the energy markets. These rules required EU member states to hit minimum storage target of 90% of their capacity before winter each year and to share the stored gas within the EU in a spirit of solidarity. In July 2025, the Council decided to extend these rules for another two years (COM/2025/99) and introduced additional flexibility to adapt to changing market conditions (European Commission, 2025). Accordingly, while the 90% fill target was maintained, it became possible to achieve this target at any time between October 1 and December 1. In addition, a 10% flexibility margin was granted to reduce difficulties in the filling process, and the Commission was given the authority to increase this margin to 5% in the event of adverse market conditions (European Council, 2026).

In terms of LNG supply, even though the likelihood of becoming dependent on a single country is considered low, the structure of the LNG market could make the EU more vulnerable to market volatility, high prices, and the decisions of external suppliers. To ensure energy security, the EU and its members seek to establish stronger ties with reliable suppliers such as Norway, the USA, and Qatar in the short-term. Nonetheless, the EU’s decarbonization objective, which targets climate neutrality by 2050, leads the Union to adopt a more restrained approach when it comes to long-term LNG contracts. Additionally, the unpredictable nature of the global LNG markets and the fact that LNG has historically been more expensive than pipeline gas are significant factors for the EU energy policy.

Given the finite nature of fossil fuels within the EU, the expansion of renewable energy sources such as solar and wind represents both strategic and necessary choice. The transition to clean energy is also a continuation of the climate targets under the Green Deal prior to the emergence of the Ukraine conflict. As an energy importer, the EU seeks to raise the share of renewable energy in its portfolio, improve energy efficiency, and encourage energy savings. The intent of these measures is to decrease fossil fuel imports, limit reliance on third-country suppliers, and strengthen the EU’s energy independence.

Conclusion

The outbreak of the Ukraine conflict has served as a powerful catalyst for rethinking of EU energy policy. It demonstrated how geopolitical conflicts could turn energy into a strategic vulnerability and stressed the dangers of overdependence on Russian natural gas. Therefore, the conflict made the structural weaknesses of the Union’s energy policy visible and highlighted the urgency of taking action. Consequently, the EU was compelled to reevaluate its energy priorities and intensify its efforts to limits its reliance on external sources.

This study has shown that, despite warning signs such as the supply disruptions experienced in 2006 and 2009, the EU’s heavy reliance on Russian gas supplies had reached a critical point before the conflict. While diversifying energy sources and suppliers had been on EU’s policy agenda for a considerable time, concrete and effective measures remained inadequate until the eruption of conflict. The conflict pushed supply security, diversification, and strategic autonomy at the top of the EU’s policy agenda. Yet, the developments that have taken place since 2022 represent not only a reaction to an immediate crisis but a broader transformation for the EU energy strategy.

To overcome these challenges, the Union has undertaken several measures aimed at reducing its dependence on Russian energy supplies. These measures range from the expansion of LNG imports, the strengthening of cooperation alternative suppliers, to the development of greater storage capacity, the promotion energy-saving policies, and acceleration in renewable energy investment. These efforts helped the EU become more resilient against price volatility and disruptions in supply. Also, it has demonstrated that energy security cannot be achieved simply by switching suppliers but requires a comprehensive restructuring of the energy approach.

In conclusion, the Ukraine conflict has revealed weaknesses in EU energy policy and exposed its strong reliance on Russian gas. As a result, the Union intensified its initiatives to move beyond diversification to include renewable energy sources and a strong commitment to energy efficiency. Decreasing reliance on fossil fuels, ensuring flexibility in the energy market, and establishing a more balanced and environmentally responsible energy portfolio will be essential in improving the EU’s capacity to handle future crises. Lasting success will depend on the effectiveness and consistency of future policies. If the Union continues to invest in and coordinate its energy transition efforts, it can lay the foundation for a more resilient, sustainable, and autonomous energy future.

Acknowledgements

The author would like to thank reviewers for their insightful comments and suggestions.

Disclosure Statement

No potential conflict of interest was reported by the author(s).

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Licensing and Repository Policy

This article is published under the Creative Commons Attribution-NonCommercial 4.0 International License (CC BY-NC 4.0). Global Geopolitics allows authors to deposit all versions of their manuscripts in an institutional or other repository of their choice without embargo.

Author Biography

Simge Pelit (ORCID iD: https://orcid.org/0000-0001-9334-6913) is a Research Assistant in the Department of International Relations at Istinye University and a PhD candidate in International Relations department at Galatasaray University. She graduated from Hacettepe University’s Department of International Relations in 2018 and completed her M.A. in International Relations at Hacettepe University in 2022 with a thesis on the European Union’s democracy promotion in Serbia. From April 2026, she will continue her doctoral research under the supervision of Prof. Annette Freyberg-Inan at the University of Amsterdam. Her research focuses on the Western Balkans, the European Union, democracy promotion, and ontological security. She is fluent in Turkish and English and has proficiency in German.

References

Agnolucci, O. & Makarenko, N. (2025). Global gas price paths diverge as LNG reshapes market balances. World Bank Blogs. https://blogs.worldbank.org/en/opendata/global-gas-price-paths-diverge-as-lng-reshapes-market-balances

Azzuni, A., & Breyer, C. (2018). Definitions and dimensions of energy security: a literature review. Wiley Interdisciplinary Reviews: Energy and Environment, 7(1), e268. https://doi.org/10.1002/wene.268

Bahgat, G. (2006). Europe’s energy security: challenges and opportunities. International Affairs, 82(5), 961–975.

Carfora, A., Pansini, R.V., & Scandurra, G. (2022). Energy dependence, renewable energy generation and import demand: Are EU countries resilient?, Renewable Energy, 195, 1262-1274.

Chow, E.C. (2009). The European Gas Crisis. Center for Strategic and International Studies-CSIS. https://www.csis.org/analysis/european-gas-crisis

Deirmentzoglou, G. A., Anastasopoulou, E. E., & Sklias, P. (2024). International economic relations and energy security in the European Union: a systematic literature review. International Journal of Sustainable Energy, 43(1). https://doi.org/10.1080/14786451.2024.2385682

Energy Charter Treaty. (2016). The International Energy Charter Consolidated Energy Charter Treaty. https://www.energycharter.org/fileadmin/DocumentsMedia/Legal/ECTC-en.pdf

European Commission. (2000). EU/Russia Summit Joint Declaration. https://ec.europa.eu/commission/presscorner/detail/en/ip_00_1239

European Commission. (2014). Communication from the Commission to the European Parliament and the Council European Energy Security Strategy COM(2014) 330 final.

European Commission. (2016). Proposal For a Regulation of the European Parliament and of the Council Concerning Measures to Safeguard the Security of Gas Supply and Repealing Regulation (EU) No 994/2010 COM(2016) 52 Final. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=consil%3AST_10377_2016_INIT

European Commission. (2022b). Joint communication to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions: EU external energy engagement in a changing world {SWD(2022) 152 final}.

European Commission. (2022c). REPowerEU: Joint European action for more affordable, secure and sustainable energy. https://ec.europa.eu/commission/presscorner/detail/en/ip_22_1511

European Commission. (2024). Liquefied natural gas. https://energy.ec.europa.eu/topics/carbon-management-and-fossil-fuels/liquefied-natural-gas_en

European Commission. (2025). Proposal for a regulation of the European Parliament and of the Council amending Regulation (EU) 2017/1938 as regards the role of gas storage for securing gas supplies ahead of the winter season (COM/2025/99 final). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:52025PC0099

European Commission. (2026). Security of Gas Supply. https://energy.ec.europa.eu/topics/energy-security/security-gas-supply_en

European Commission. (n.d.). Diversification of gas supply sources and routes. https://energy.ec.europa.eu/topics/energy-security/diversification-gas-supply-sources-and-routes_en

European Council. (2023b). Where does the EU’s gas come from?. https://www.consilium.europa.eu/en/infographics/eu-gas-supply/#:~:text=Norway%20and%20the%20United%20States,countries%2C%20the%20UK%20and%20Qatar.&text=Treemap%20showing%20market%20shares%20and,to%20the%20EU%20in%202023

European Council. (2024). Refugees from Ukraine in the EU. https://www.consilium.europa.eu/en/infographics/ukraine-refugees-eu/

European Council. (2026). How much gas have the EU countries stored?. https://www.consilium.europa.eu/en/infographics/gas-storage-capacity/#0

European Parliament. (2023a). EU energy security and the war in Ukraine: From sprint to marathon. https://www.europarl.europa.eu/thinktank/en/document/EPRS_BRI(2023)739362

European Parliament. (2023b). Question Time: How to ensure energy security in the EU in 2023. https://www.europarl.europa.eu/thinktank/en/document/EPRS_ATA(2023)739376

European Parliament. (2024). Energy policy: general principles. https://www.europarl.europa.eu/factsheets/en/sheet/68/energy-policy-general-principles

Eurostat. (2022a). Energy dependency rate, EU, 2010-2020. https://ec.europa.eu/eurostat/statistics-explained/index.php?title=File:Energy_dependency_rate,_EU,_2010-2020_(%25).png

Eurostat. (2022b). Main origin of primary energy imports, EU, 2010-2020. https://ec.europa.eu/eurostat/statistics-explained/index.php?title=File:Main_origin_of_primary_energy_imports,_EU,_2010-2020_(%25_of_EU_imports)_v6.png

Eurostat. (2022c). Key Figures on Europe 2022 edition. https://ec.europa.eu/eurostat/documents/3217494/14871939/KS-EI-22-001-EN-N.pdf/9ad193b2-fb0e-7ef3-2200-053f845df1be?t=1657630160989

Eurostat. (2026). EU imports of energy products - latest developments. https://ec.europa.eu/eurostat/statistics-explained/index.php?title=EU_imports_of_energy_products_-_latest_developments

Eurostat. (n.d.). Glossary: Energy dependency rate. https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Glossary:Energy_dependency_rate#:~:text=The%20energy%20dependency%20rate%20shows,energy%2C%20expressed%20as%20a%20percentage

Güven, H., & Güneş, D. (2020). Avrupa Birliği enerji politikaları. In A. Kaya, S. Aydın-Düzgit, Y. Gürsoy, & Ö. Onursal Beşgül (Eds.), Avrupa Birliği’ne giriş (pp. 269-284). İstanbul Bilgi Üniversitesi Yayınları.

International Energy Agency (IEA). (2019). Energy security Ensuring the uninterrupted availability of energy sources at an affordable price. https://downloads.regulations.gov/EPA-HQ-OAR-2022-0829-0228/attachment_22.pdf

International Energy Agency (IEA). (n.d.a). Glossary. https://www.iea.org/glossary#energy-security

Kanellakis, M., Martinopoulos, G., & Zachariadis, T. (2013). European energy policy—A review. Energy Policy, 62, 1020-1030. https://doi.org/10.1016/J.ENPOL.2013.08.008

LaBelle, M. C. (2024). Breaking the era of energy interdependence in Europe: A multidimensional reframing of energy security, sovereignty, and solidarity. Energy Strategy Reviews, 52, 101314. https://doi.org/10.1016/j.esr.2024.101314

Lisbon Treaty. (2008). Consolidated Version of the Treaty on European Union. https://eur-lex.europa.eu/resource.html?uri=cellar:2bf140bf-a3f8-4ab2-b506-fd71826e6da6.0023.02/DOC_1&format=PDF

Muhibbiin, S. S., Tampubolon, S. T. R., & Wahyudi, V. A. P. (2025). The European Union’s efforts to formulate energy policy following the 2022–2023 Russian invasion of Ukraine. In Proceedings of IROFONIC 2025: Global initiatives for sustainable development goals.

Osička, J., & Černoch, F. (2022). European energy politics after Ukraine: The road ahead. Energy Research & Social Science, 91. https://doi.org/10.1016/j.erss.2022.102757

Roa, T.G. (2026). From vulnerability to strategic autonomy: Discursive transformations in EU energy security (2003–2024), Energy Strategy Reviews, 64, 1-11. 10.1016/j.esr.2026.102113

Sauvageot, E.P. (2020). Between Russia as producer and Ukraine as a transit country: EU dilemma of interdependence and energy security. Energy Policy, 145. https://doi.org/10.1016/j.enpol.2020.111699

Skalamera, M. (2015). The Ukraine Crisis: The Neglected Gas Factor. Orbis, 59(3), 398-410. https://doi.org/10.1016/J.ORBIS.2015.05.002

Sözen, A. (2009). Future projection of the energy dependency of Turkey using artificial neural network. Energy Policy, 37, 4827-4833. https://doi.org/10.1016/J.ENPOL.2009.06.040

Tekin, A. & Williams, P.A. (2011). Evolution of EU Energy Policy. In: Geo-Politics of the Euro-Asia Energy Nexus (pp.13-36). Palgrave Macmillan. https://doi.org/10.1057/9780230294943_2

Tóth, B., Kotek, P., & Selei, A. (2020). Rerouting Europe's gas transit landscape - Effects of Russian natural gas infrastructure strategy on the V4. Energy Policy, 146, 111748. https://doi.org/10.1016/j.enpol.2020.111748

U.S. Energy Information Agency. (2022). What Is Price Volatility?. https://www.eia.gov/naturalgas/weekly/archivenew_ngwu/2003/10_23/volatility%2010-22-03.htm#:~:text=The%20term%20%E2%80%9Cprice%20volatility%E2%80%9D%20is,prices%2C%20defines%20a%20volatile%20market

Yafimava, K. (2011). The Transit Dimension of EU Energy Security: Russian Gas Transit across Ukraine, Belarus, and Moldova. Oxford University Press.

Yergin, D. (2006). Ensuring energy security. Foreign Affairs, 85(2), 69–82.